To demonstrate the use of the FKF package this example

shows how to fit an ARMA(2, 1) model using this Kalman filter

implimentation and teh extraction of the resulting filtered and smoothed

estimates.

Start by loading the package:

Estimation

To estimate the parameters using numerical optimisation two functions are specified. The first creates a state space representation out of the four ARMA parameters

arma21ss <- function(ar1, ar2, ma1, sigma) {

Tt <- matrix(c(ar1, ar2, 1, 0), ncol = 2)

Zt <- matrix(c(1, 0), ncol = 2)

ct <- matrix(0)

dt <- matrix(0, nrow = 2)

GGt <- matrix(0)

H <- matrix(c(1, ma1), nrow = 2) * sigma

HHt <- H %*% t(H)

a0 <- c(0, 0)

P0 <- matrix(1e6, nrow = 2, ncol = 2)

return(list(a0 = a0, P0 = P0, ct = ct, dt = dt, Zt = Zt, Tt = Tt, GGt = GGt,

HHt = HHt))

}The second is the objective function passed to optim

which returns the noegative log-likelihood

objective <- function(theta, yt) {

sp <- arma21ss(theta["ar1"], theta["ar2"], theta["ma1"], theta["sigma"])

ans <- fkf(a0 = sp$a0, P0 = sp$P0, dt = sp$dt, ct = sp$ct, Tt = sp$Tt,

Zt = sp$Zt, HHt = sp$HHt, GGt = sp$GGt, yt = yt)

return(-ans$logLik)

}Estimation is then performed using a numeric search by

optim

Results

First consider the 95% CI for the parameter estimate which can be constructed using the hessian of the fit:

## Confidence intervals

p <- cbind(actual = c(ar1=ar1,ar2=ar2,ma1=ma1,sigma=sigma),

estimate = fit$par,

lowerCI = fit$par - qnorm(0.975) * sqrt(diag(solve(fit$hessian))),

upperCI = fit$par + qnorm(0.975) * sqrt(diag(solve(fit$hessian))))

p

#> actual estimate lowerCI upperCI

#> ar1 0.600000 0.44220027 0.2483370 0.6360635

#> ar2 0.200000 0.27865796 0.1527385 0.4045774

#> ma1 -0.200000 -0.01510979 -0.2157122 0.1854926

#> sigma 1.414214 1.41943609 1.3571952 1.4816770showing the actual parameters fall within the 95% CI of the estimated values.

The series can be filtered using the estimated parameter values

sp <- arma21ss(fit$par["ar1"], fit$par["ar2"], fit$par["ma1"], fit$par["sigma"])

ans <- fkf(a0 = sp$a0, P0 = sp$P0, dt = sp$dt, ct = sp$ct, Tt = sp$Tt,

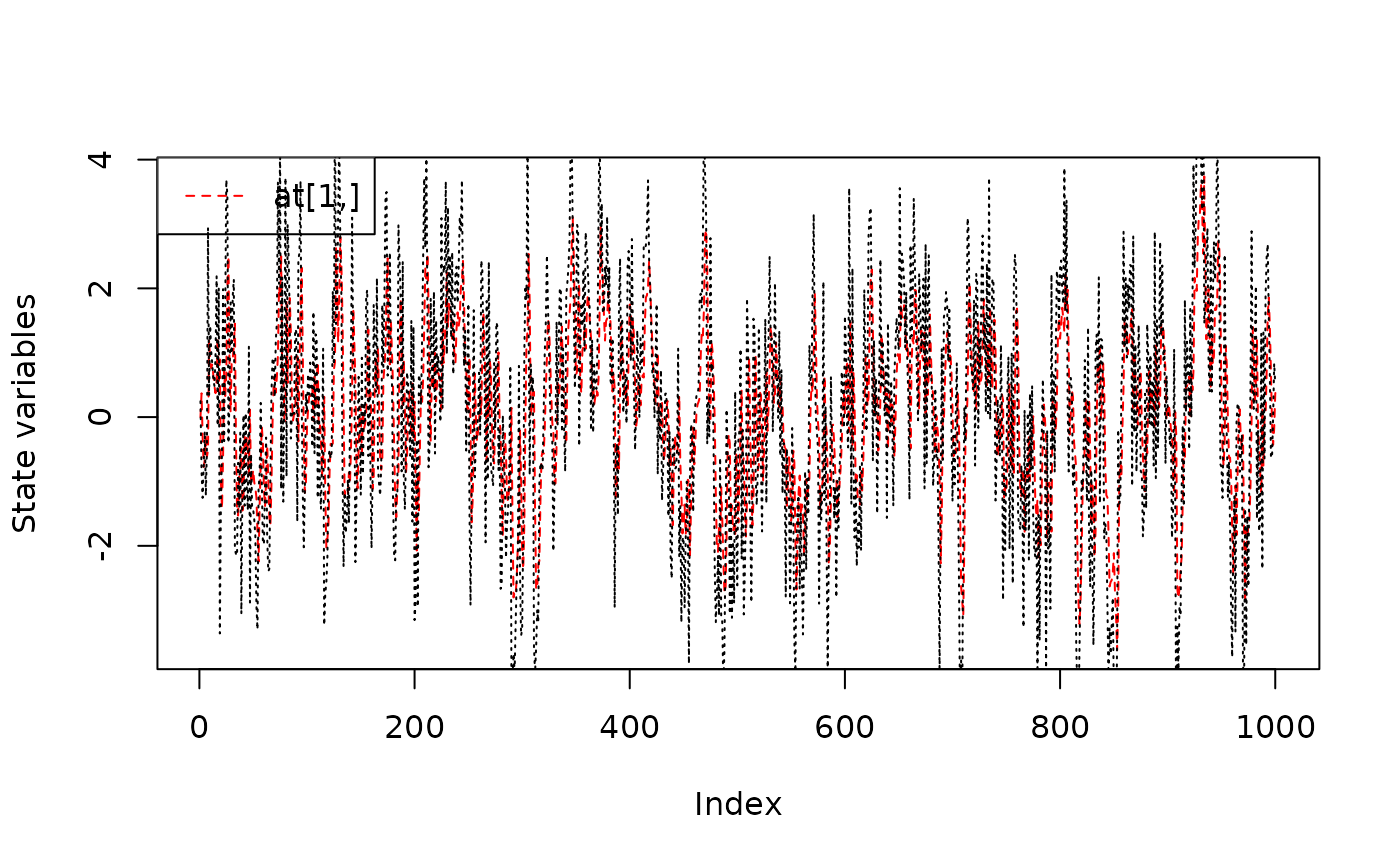

Zt = sp$Zt, HHt = sp$HHt, GGt = sp$GGt, yt = rbind(a))This allows comparision of the prediction with the realization

and comparision of the filtered series with the realization

and comparision of the filtered series with the realization

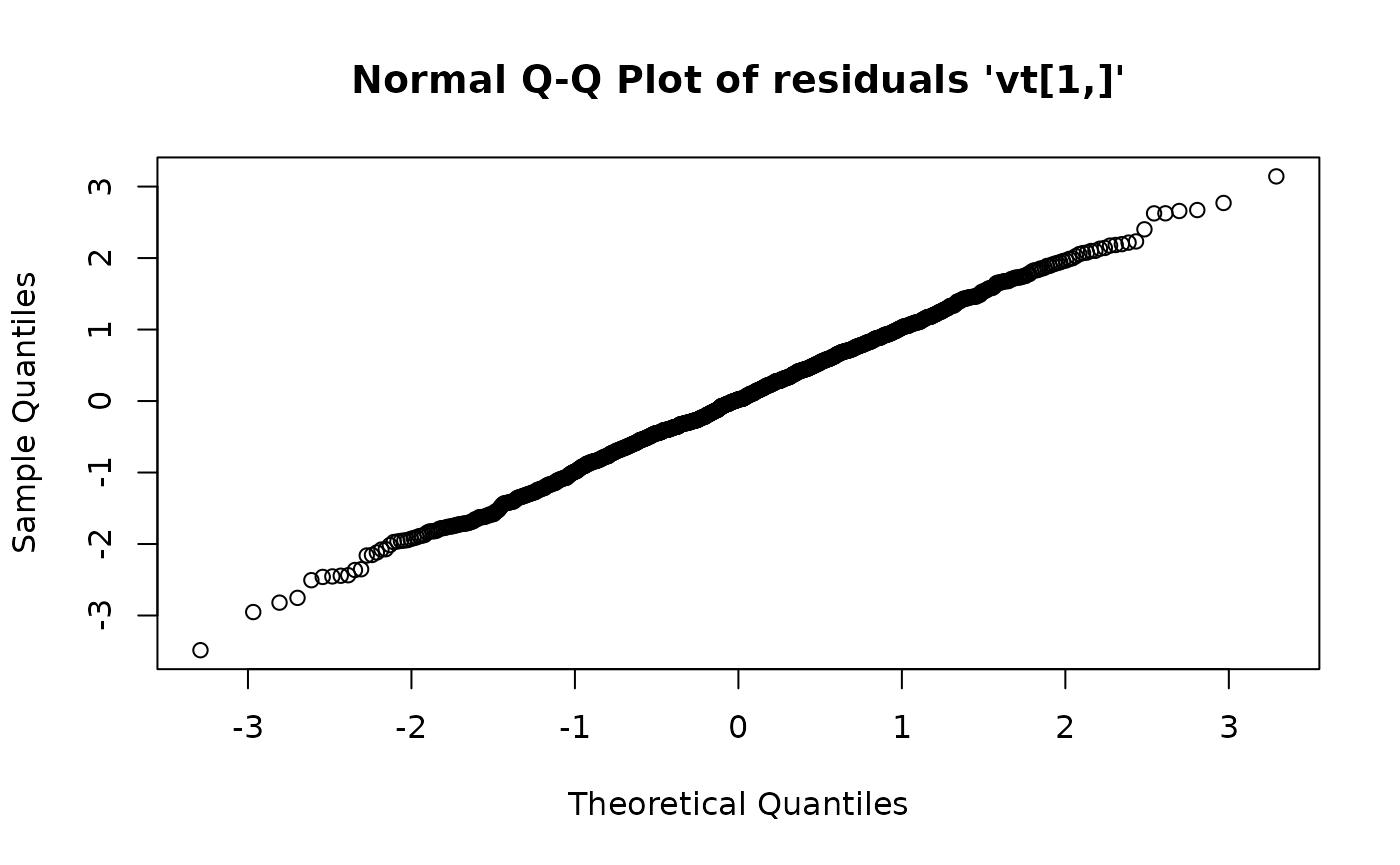

The plotting function for the fkf class also allows visual checking of whether the residuals are Gaussian

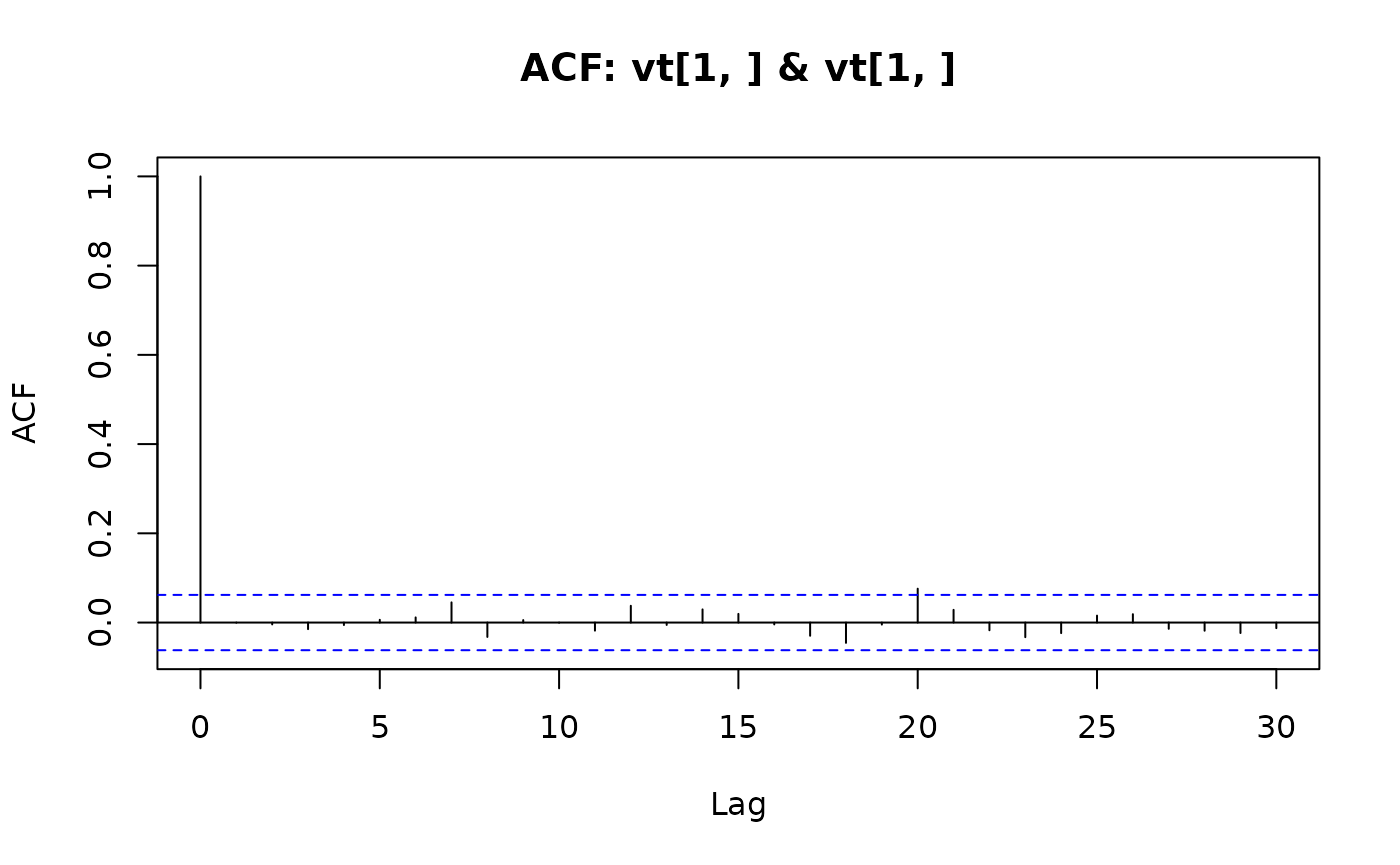

plot(ans, type = "resid.qq") or if there is a linear serial dependence through ‘acf’

or if there is a linear serial dependence through ‘acf’

plot(ans, type = "acf")

The smoothed estimates can also be computed by a simple call to fks

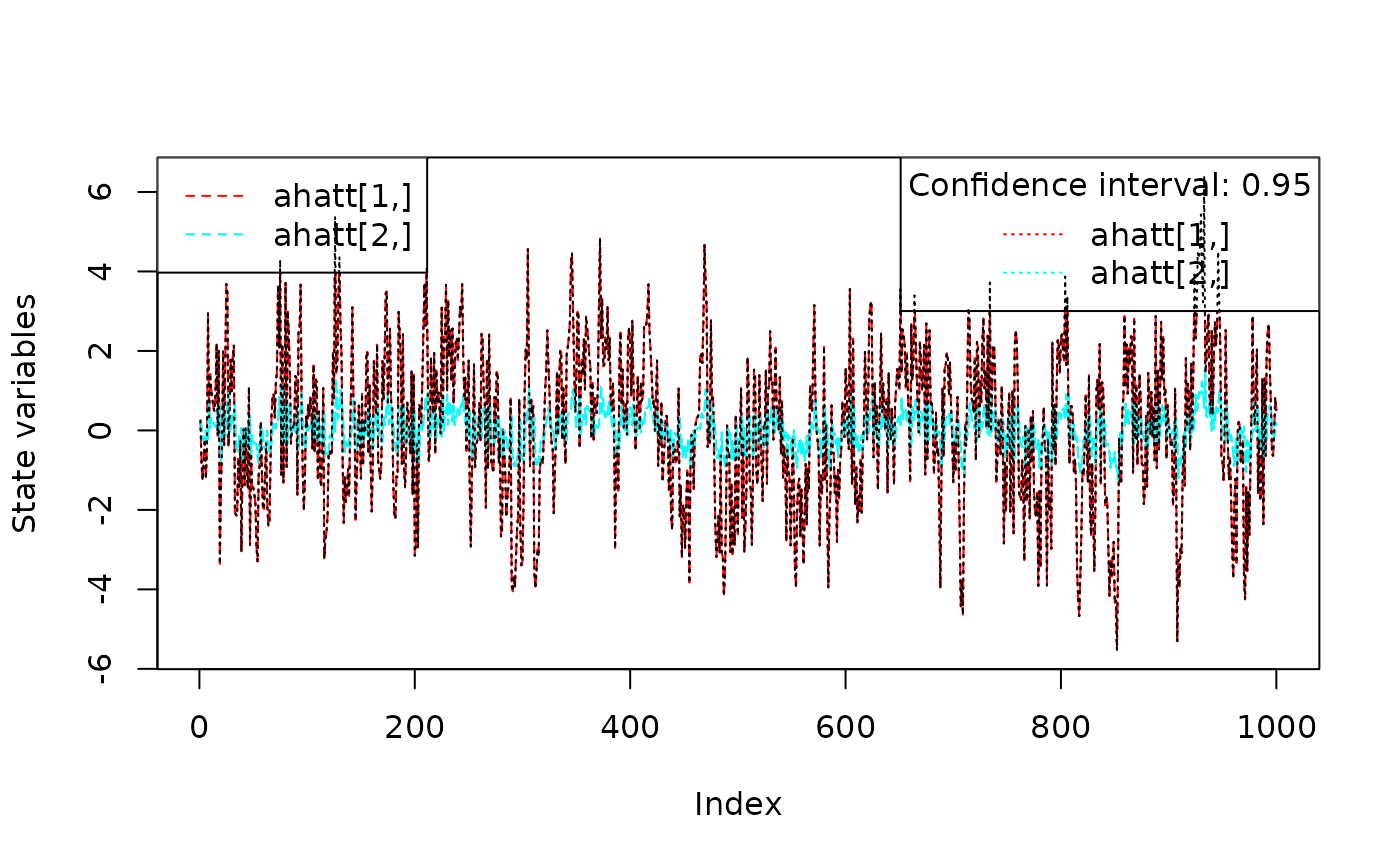

sm <- fks(ans)The smoothed estiamte with confidence intervals can be plotted alongside the observed data