This function allows for fast and flexible Kalman filtering. Both, the

measurement and transition equation may be multivariate and parameters

are allowed to be time-varying. In addition “NA”-values in the

observations are supported. fkf wraps the C-function

FKF which fully relies on linear algebra subroutines contained

in BLAS and LAPACK.

fkf(a0, P0, dt, ct, Tt, Zt, HHt, GGt, yt)Arguments

- a0

A

vectorgiving the initial value/estimation of the state variable.- P0

A

matrixgiving the variance ofa0.- dt

A

matrixgiving the intercept of the transition equation (see Details).- ct

A

matrixgiving the intercept of the measurement equation (see Details).- Tt

An

arraygiving the factor of the transition equation (see Details).- Zt

An

arraygiving the factor of the measurement equation (see Details).- HHt

An

arraygiving the variance of the innovations of the transition equation (see Details).- GGt

An

arraygiving the variance of the disturbances of the measurement equation (see Details).- yt

A

matrixcontaining the observations. “NA”-values are allowed (see Details).

Value

An S3-object of class “fkf”, which is a list with the following elements:

att | A \(m \times n\)-matrix containing the filtered state variables, i.e. att[,t] = \(a_{t|t}\). |

at | A \(m \times (n + 1)\)-matrix containing the predicted state variables, i.e. at[,t] = \(a_t\). |

Ptt | A \(m \times m \times n\)-array containing the variance of att, i.e. Ptt[,,t] = \(P_{t|t}\). |

Pt | A \(m \times m \times (n + 1)\)-array containing the variances of at, i.e. Pt[,,t] = \(P_t\). |

vt | A \(d \times n\)-matrix of the prediction errors i.e. vt[,t] = \(v_t\). |

Ft | A \(d \times d \times n\)-array which contains the variances of vt, i.e. Ft[,,t] = \(F_t\). |

Kt | A \(m \times d \times n\)-array containing the “Kalman gain” i.e. Kt[,,t] = \(k_t\). |

logLik | The log-likelihood. |

status | A vector which contains the status of LAPACK's dpotri and dpotrf. \((0, 0)\) means successful exit. |

sys.time | The time elapsed as an object of class “proc_time”. |

Details

State space form

The following notation is closest to the one of Koopman et al. The state space model is represented by the transition equation and the measurement equation. Let \(m\) be the dimension of the state variable, \(d\) be the dimension of the observations, and \(n\) the number of observations. The transition equation and the measurement equation are given by $$\alpha_{t + 1} = d_t + T_t \cdot \alpha_t + H_t \cdot \eta_t$$ $$y_t = c_t + Z_t \cdot \alpha_t + G_t \cdot \epsilon_t,$$ where \(\eta_t\) and \(\epsilon_t\) are iid \(N(0, I_m)\) and iid \(N(0, I_d)\), respectively, and \(\alpha_t\) denotes the state variable. The parameters admit the following dimensions:

| \(\alpha_{t} \in R^{m}\) | \(d_{t} \in R^m\) | \(\eta_{t} \in R^m\) |

| \(T_{t} \in R^{m \times m}\) | \(H_{t} \in R^{m \times m}\) | |

| \(y_{t} \in R^d\) | \(c_t \in R^d\) | \(\epsilon_{t} \in R^d\) |

| \(Z_{t} \in R^{d \times m}\) | \(G_{t} \in R^{d \times d}\) |

Note that fkf takes as input HHt and GGt which

corresponds to \(H_t H_t^\prime\) and \(G_t G_t^\prime\).

Iteration:

The filter iterations are implemented using the expected values $$a_{t} = E[\alpha_t | y_1,\ldots,y_{t-1}]$$ $$a_{t|t} = E[\alpha_t | y_1,\ldots,y_{t}]$$

and variances $$P_{t} = Var[\alpha_t | y_1,\ldots,y_{t-1}]$$ $$P_{t|t} = Var[\alpha_t | y_1,\ldots,y_{t}]$$

of the state \(\alpha_{t}\) in the following way (for the case of no NA's):

Initialisation: Set \(t=1\) with \(a_{t} = a0\) and \(P_{t}=P0\)

Updating equations: $$v_t = y_t - c_t - Z_t a_t$$ $$F_t = Z_t P_t Z_t^{\prime} + G_t G_t^\prime$$ $$K_t = P_t Z_t^{\prime} F_{t}^{-1}$$ $$a_{t|t} = a_t + K_t v_t$$ $$P_{t|t} = P_t - P_t Z_t^\prime K_t^\prime$$

Prediction equations: $$a_{t+1} = d_{t} + T_{t} a_{t|t}$$ $$P_{t+1} = T_{t} P_{t|t} T_{t}^{\prime} + H_t H_t^\prime$$

Next iteration: Set \(t=t+1\) and goto “Updating equations”.

NA-values:

NA-values in the observation matrix yt are supported. If

particular observations yt[,i] contain NAs, the NA-values are

removed and the measurement equation is adjusted accordingly. When

the full vector yt[,i] is missing the Kalman filter reduces to

a prediction step.

Parameters:

The parameters can either be constant or deterministic time-varying. Assume the number of observations is \(n\) (i.e. \(y = (y_t)_{t = 1, \ldots, n}, y_t = (y_{t1}, \ldots, y_{td})\)). Then, the parameters admit the following classes and dimensions:

dt | either a \(m \times n\) (time-varying) or a \(m \times 1\) (constant) matrix. |

Tt | either a \(m \times m \times n\) or a \(m \times m \times 1\) array. |

HHt | either a \(m \times m \times n\) or a \(m \times m \times 1\) array. |

ct | either a \(d \times n\) or a \(d \times 1\) matrix. |

Zt | either a \(d \times m \times n\) or a \(d \times m \times 1\) array. |

GGt | either a \(d \times d \times n\) or a \(d \times d \times 1\) array. |

yt | a \(d \times n\) matrix. |

BLAS and LAPACK routines used:

The R function fkf basically wraps the C-function

FKF, which entirely relies on linear algebra subroutines

provided by BLAS and LAPACK. The following functions are used:

| BLAS: | dcopy, dgemm, daxpy. |

| LAPACK: | dpotri, dpotrf. |

FKF is called through the .Call interface. Internally,

FKF extracts the dimensions, allocates memory, and initializes

the R-objects to be returned. FKF subsequently calls

cfkf which performs the Kalman filtering.

The only critical part is to compute the inverse of \(F_t\)

and the determinant of \(F_t\). If the inverse can not be

computed, the filter stops and returns the corresponding message in

status (see Value). If the computation of the

determinant fails, the filter will continue, but the log-likelihood

(element logLik) will be “NA”.

The inverse is computed in two steps:

First, the Cholesky factorization of \(F_t\) is

calculated by dpotrf. Second, dpotri calculates the

inverse based on the output of dpotrf.

The determinant of \(F_t\) is computed using again the

Cholesky decomposition.

The first element of both at and Pt is filled with the

function arguments a0 and P0, and the last, i.e. the (n +

1)-th, element of at and Pt contains the predictions for the next time step.

References

Harvey, Andrew C. (1990). Forecasting, Structural Time Series Models and the Kalman Filter. Cambridge University Press.

Hamilton, James D. (1994). Time Series Analysis. Princeton University Press.

Koopman, S. J., Shephard, N., Doornik, J. A. (1999). Statistical algorithms for models in state space using SsfPack 2.2. Econometrics Journal, Royal Economic Society, vol. 2(1), pages 107-160.

See also

Examples

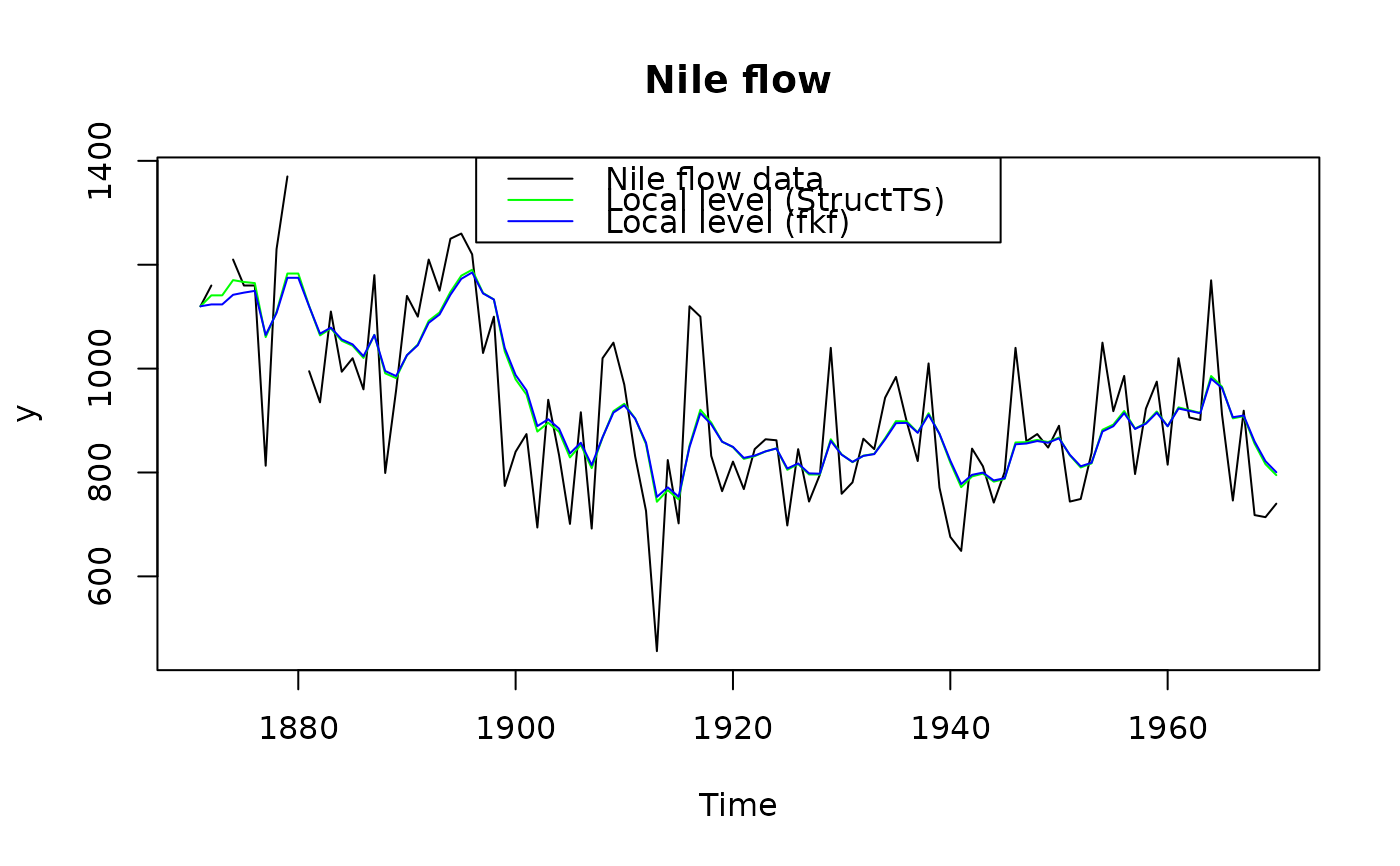

## <--------------------------------------------------------------------------->

## Example: Local level model for the Nile's annual flow.

## <--------------------------------------------------------------------------->

## Transition equation:

## alpha[t+1] = alpha[t] + eta[t], eta[t] ~ N(0, HHt)

## Measurement equation:

## y[t] = alpha[t] + eps[t], eps[t] ~ N(0, GGt)

y <- Nile

y[c(3, 10)] <- NA # NA values can be handled

## Set constant parameters:

dt <- ct <- matrix(0)

Zt <- Tt <- matrix(1)

a0 <- y[1] # Estimation of the first year flow

P0 <- matrix(100) # Variance of 'a0'

## Estimate parameters:

fit.fkf <- optim(c(HHt = var(y, na.rm = TRUE) * .5,

GGt = var(y, na.rm = TRUE) * .5),

fn = function(par, ...)

-fkf(HHt = matrix(par[1]), GGt = matrix(par[2]), ...)$logLik,

yt = rbind(y), a0 = a0, P0 = P0, dt = dt, ct = ct,

Zt = Zt, Tt = Tt)

## Filter Nile data with estimated parameters:

fkf.obj <- fkf(a0, P0, dt, ct, Tt, Zt, HHt = matrix(fit.fkf$par[1]),

GGt = matrix(fit.fkf$par[2]), yt = rbind(y))

## Compare with the stats' structural time series implementation:

fit.stats <- StructTS(y, type = "level")

fit.fkf$par

#> HHt GGt

#> 1385.066 15124.131

fit.stats$coef

#> level epsilon

#> 1599.452 14904.781

## Plot the flow data together with fitted local levels:

plot(y, main = "Nile flow")

lines(fitted(fit.stats), col = "green")

lines(ts(fkf.obj$att[1, ], start = start(y), frequency = frequency(y)), col = "blue")

legend("top", c("Nile flow data", "Local level (StructTS)", "Local level (fkf)"),

col = c("black", "green", "blue"), lty = 1)