This function can be run after running fkf to produce

"smoothed" estimates of the state variable \(\alpha_t\).

Unlike the output of the filter, these estimates are conditional

on the entire set of \(n\) data points rather than only the past, see details.

fks(FKFobj)Arguments

- FKFobj

An S3-object of class "fkf", returned by

fkf.

Value

An S3-object of class "fks" which is a list with the following elements:

ahatt A \(m \times n\)-matrix containing the

smoothed state variables, i.e. ahatt[,t] = \(a_{t|n}\)Vt A \(m \times m \times n\)-array

containing the variances of ahatt, i.e. Vt[,,t] = \(P_{t|n}\)

Details

The following notation is taken from the fkf function descriptions

and is close to the one of Koopman et al. The smoother estimates

$$a_{t|n} = E[\alpha_{t} | y_1,\ldots,y_n]$$

$$P_{t|n} = Var[\alpha_{t} | y_1,\ldots,y_n]$$

based on the outputs of the forward filtering pass performed by fkf.

The formulation of Koopman and Durbin is used which evolves the two values \(r_{t} \in R^m\) and \(N_{t} \in R^{m \times m}\) to avoid inverting the covariance matrix.

Iteration:

If there are no missing values the iteration proceeds as follows:

Initialisation: Set \(t=n\), with \(r_t =0\) and \(N_t =0\).

Evolution equations: $$L = T_{t} - T_{t}K_{t}Z_{t}$$ $$r_{t-1} = Z_{t}^\prime F_{t}^{-1} v_{t} + L^\prime r_{t}$$ $$N_{t-1} = Z_{t}^\prime F_{t}^{-1} Z_{t} + L^\prime N_{t} L$$

Updating equations: $$a_{t|n} = a_{t|t-1} + P_{t|t-1}r_{t-1}$$ $$P_{t|n} = P_{t|t-1} - P_{t|t-1}N_{t-1}P_{t|t-1}$$

Next iteration: Set \(t=t-1\) and goto “Evolution equations”.

References

Koopman, S. J. and Durbin, J. (2000). Fast filtering and smoothing for multivariate state space models Journal of Time Series Analysis Vol. 21, No. 3

Examples

## <--------------------------------------------------------------------------->

## Example: Local level model for the Nile's annual flow.

## <--------------------------------------------------------------------------->

## Transition equation:

## alpha[t+1] = alpha[t] + eta[t], eta[t] ~ N(0, HHt)

## Measurement equation:

## y[t] = alpha[t] + eps[t], eps[t] ~ N(0, GGt)

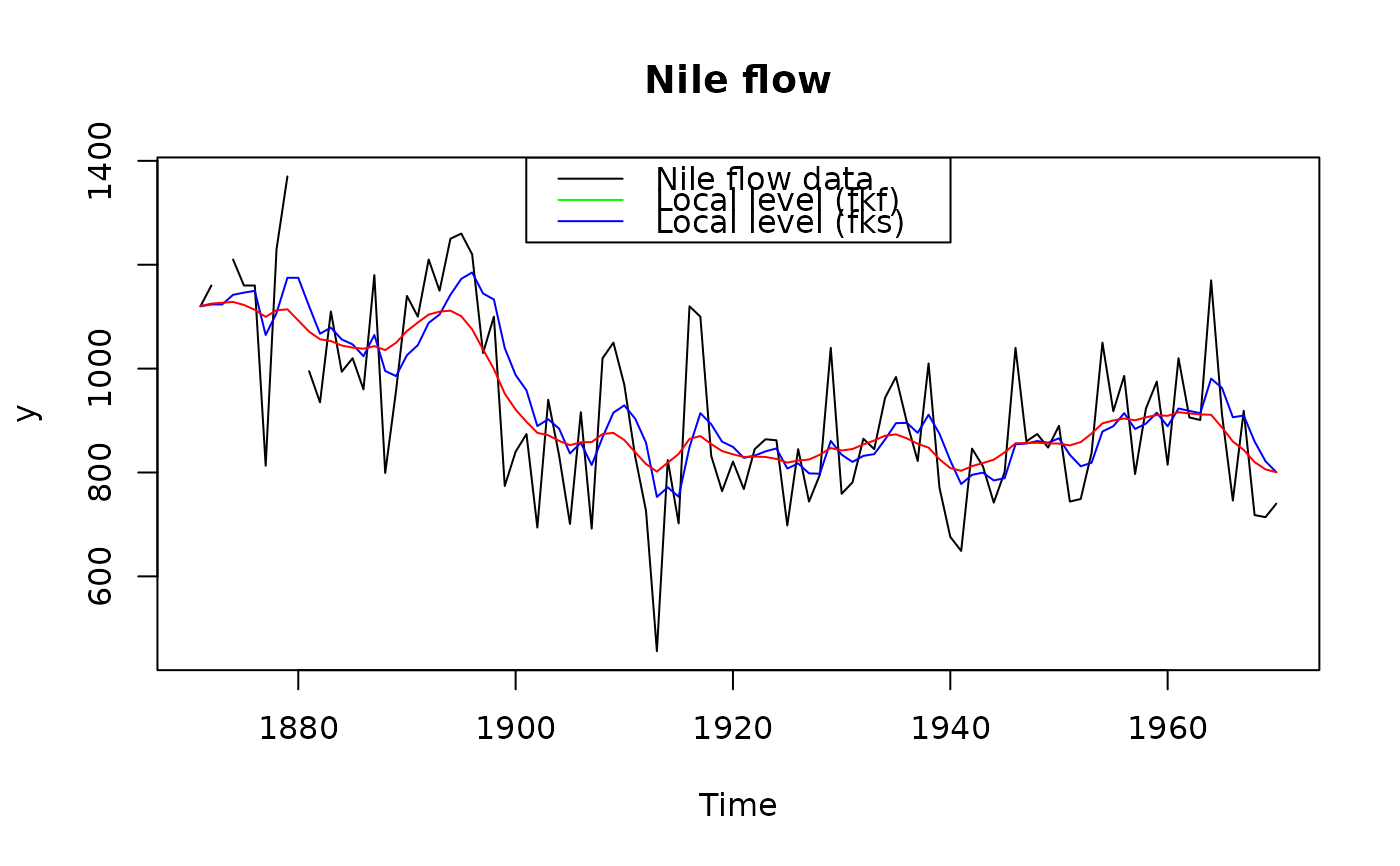

y <- Nile

y[c(3, 10)] <- NA # NA values can be handled

## Set constant parameters:

dt <- ct <- matrix(0)

Zt <- Tt <- matrix(1)

a0 <- y[1] # Estimation of the first year flow

P0 <- matrix(100) # Variance of 'a0'

## Estimate parameters:

fit.fkf <- optim(c(HHt = var(y, na.rm = TRUE) * .5,

GGt = var(y, na.rm = TRUE) * .5),

fn = function(par, ...)

-fkf(HHt = matrix(par[1]), GGt = matrix(par[2]), ...)$logLik,

yt = rbind(y), a0 = a0, P0 = P0, dt = dt, ct = ct,

Zt = Zt, Tt = Tt)

## Filter Nile data with estimated parameters:

fkf.obj <- fkf(a0, P0, dt, ct, Tt, Zt, HHt = matrix(fit.fkf$par[1]),

GGt = matrix(fit.fkf$par[2]), yt = rbind(y))

## Smooth the data based on the filter object

fks.obj <- fks(fkf.obj)

## Plot the flow data together with local levels:

plot(y, main = "Nile flow")

lines(ts(fkf.obj$att[1, ], start = start(y), frequency = frequency(y)), col = "blue")

lines(ts(fks.obj$ahatt[1,], start = start(y), frequency = frequency(y)), col = "red")

legend("top", c("Nile flow data", "Local level (fkf)","Local level (fks)"),

col = c("black", "green", "blue", "red"), lty = 1)